The Hidden Tradeoffs of Staying Put: Is Your Low Mortgage Rate Keeping You Stuck?

It’s easy to stay put when your mortgage rate feels like a win. Low rates create comfort and for many homeowners, that comfort turns into hesitation about moving.

If you bought or refinanced during the pandemic-era rate drop, you likely locked in a historically low number. In 2021, rates hit record lows near 2.65% [1], and even today, more than half of homeowners are still below 4% [2]. This has fueled what’s known as the “lock-in effect,” where homeowners delay moving simply to preserve their current rate.

And understandably so. When you’re holding a 3% or 4% mortgage, the idea of moving into today’s higher-rate environment can feel like a financial step backward.

Recent surveys show just how strong that feeling is: about one in four homeowners with sub-5% rates say nothing could convince them to give up their current mortgage, and another quarter would only consider it if they received $200,000 or more in compensation [3]. But those reactions are often driven more by emotion than by a full financial comparison.

What if the real tradeoff looks different when you zoom out—beyond the rate itself and into how it impacts your lifestyle, timing, and long-term financial options?

The lifestyle cost of staying in place

Money isn’t the only factor impacted by staying in a home that no longer fits your life.

Maybe your “home office” is actually a corner of your bedroom, making it harder to separate work and personal life. Maybe your commute has doubled after a job change, taking hours each week away from family or rest. Or maybe you’re paying for storage because your home no longer has enough space.

These aren’t just inconveniences—they slowly shape your day-to-day life. Over time, they can add up in stress, energy, and lost flexibility.

The cost of waiting in a rising market

It’s important to remember that today’s historically low rates were an exception, not the norm.

Most economists don’t expect a return to pandemic-era rates anytime soon. That means waiting for “better rates” may come with a different cost: higher home prices.

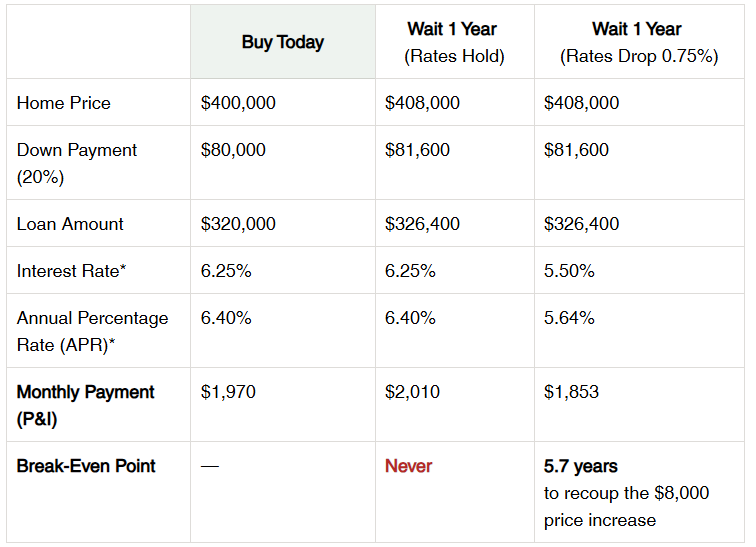

In many markets, home values continue to rise (though appreciation varies by location). For example, a $400,000 home today with just 2% annual appreciation could cost $408,000 next year. Even if interest rates improve slightly, that price increase can offset the savings.

Here’s what that comparison might look like:

What this shows is simple: even if rates improve later, rising prices can erase much of the benefit—or delay the financial break-even point for years.

*The sample rates shown are neither an advertisement, an estimate, nor an offer to lend. Rates are for illustrative purposes only and do not represent actual terms being offered. The annual percentage rate (APR) is the cost of credit over the term of the loan expressed as an annual rate. The APR shown assumes a 1% origination fee, $1,000 in other fees, and pre-paid (per diem) interest calculated at the 30-year fixed mortgage rate for 15 days. Monthly payment reflects principal and interest only and does not include applicable taxes and insurance. Rates, terms, and eligibility vary by borrower and are subject to change. This is not a commitment to lend.

The hidden value of home equity

It’s easy to focus on the interest rate alone, but that’s only one piece of the equation. Many homeowners are sitting on a much larger opportunity: equity. Across the country, homeowners collectively hold trillions in equity, with the average homeowner having well over $300,000 [4]. That equity can become a powerful tool when moving into a new home.

For example, putting $200,000 toward a $500,000 home creates a 40% down payment, reducing the loan amount to $300,000. At a 6.25% interest rate (APR 6.40%), the estimated monthly principal and interest would be about $1,847—less than the $1,970 payment on a $400,000 home with only 20% down.

That’s the power of equity:

A higher-priced home. A potentially lower monthly payment.

Equity doesn’t just help you buy—it creates flexibility. It can reduce monthly costs, expand your options, or even be used strategically to buy down your rate from day one.

Looking at the full picture

Financial decisions around housing are rarely just financial. They’re emotional, practical, and deeply personal. Holding onto a low interest rate feels logical and in many cases, it is. But the important question is whether that rate is still serving your life today, or quietly limiting your options.

Sometimes, moving—even into a higher rate environment can create more financial and lifestyle flexibility than staying put. That doesn’t make it the right move for everyone. But it does mean the decision is worth evaluating with complete information, not just the interest rate alone.

Bottom Line

If you’re curious what this looks like in your specific situation, a Greenway Mortgage Loan Officer can walk you through the actual numbers. Sometimes a clearer picture makes the decision much easier.

Contact us today 888-616-9885.

.png)

*The sample rates shown are neither an advertisement, an estimate, nor an offer to lend. Rates are for illustrative purposes only and do not represent actual terms being offered. The annual percentage rate (APR) is the cost of credit over the term of the loan expressed as an annual rate. The APR shown assumes a 1% origination fee, $1,000 in other fees, and pre-paid (per diem) interest calculated at the 30-year fixed mortgage rate for 15 days. Monthly payment reflects principal and interest only and does not include applicable taxes and insurance. Rates, terms, and eligibility vary by borrower and are subject to change. This is not a commitment to lend.

Sources:

[1] Freddie Mac, Primary Mortgage Market Survey.

[2] ICE Mortgage Monitor, February 2026.

[3] Storable’s 2026 Moving Forecast.

[4] ICE Mortgage Monitor, March 2026.